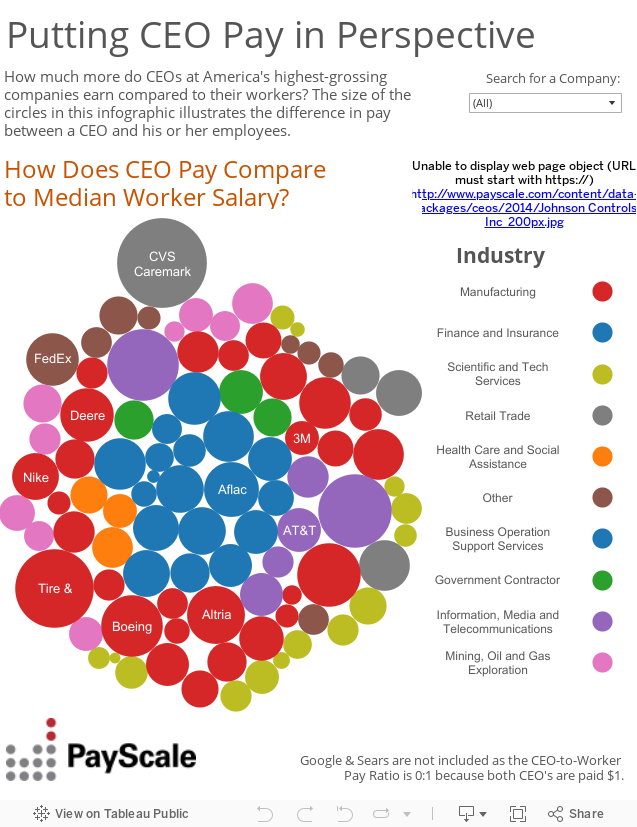

Why are American CEOs paid such obscene amounts of money? Most of them make over 150 times more than their average employee. In the Washington DC area, CEO salaries are rising faster than the national average. One CEO made $68M but his company lost $670M. How do they get such lucrative pay packages? Why do shareholders not control CEO salary?

Unfortunately, we, the retail investor, are part of the problem. Corporate boards set executives pay and board members are supposed to act on behalf of shareholders. But most board members were or are executives and it is to their advantage to have executives salaries go up. Many board members were appointed based on recommendations from the CEO they are supposed to be supervising. A basket full of conflicts of interest, right?

Shareholders could elect new board members who will moderate CEO salaries and make sure they are not highly paid in spite of poor performance, which is another big problem. But the largest blocks of shares are now held by mutual funds, ETFs, and pension funds. The mutual fund giants, Fidelity and Vanguard, do not actively vote their shares to fix the inequity in CEO pay. They basically buy advice from a "proxy advisor" like ISS who usually tells them to do what management wants. Management usually wants more pay for themselves independent of performance, so nothing is done about CEO pay. The New York Times has written this up in an article. I actually wrote to Vanguard a few years ago to complain about exactly this issue. The reply was polite and contained their voting record (almost universal support for management) but basically said that they would continue to use proxy advisors.

So until this wicked conflict of interest circle in the corporate boards is broken, we will continue to see ridiculous pay. You should write to your mutual fund company to complain as I did, without them, it is unlikely that the problem will be addressed.